Nevertheless, for 2023 I believe this range on the 10-yr yield would be ideal, taking into consideration the labor marketplace is however sound. If the labor current market starts to get even worse — this means jobless statements rise with some speed — the original assortment of this forecast will break, and bond yields will go decrease. The facts is not there yet to even have that dialogue.

From my 2023 housing industry forecast: “For 2023, the 10-year produce is at present at 3.70% and I consider the 10-yr produce range this calendar year will be involving 3.21%-4.25% as very long as the overall economy stays business. Now if the economic climate receives weaker, in particular in phrases of the labor market place breaking, which for me is jobless promises soaring to 323,000 and beyond, then we can get as reduced as 2.73% on the 10-year produce.

“With that 10-year produce vary (3.21%-4.25%), house loan prices need to be in between 5.25%-7.25%. This assumes that the spreads are vast and pricing for mortgages is however weak. On the other hand, if the spreads get better, we could even see home loan prices less than 5% if the 10-12 months yield breaks beneath 3%.”

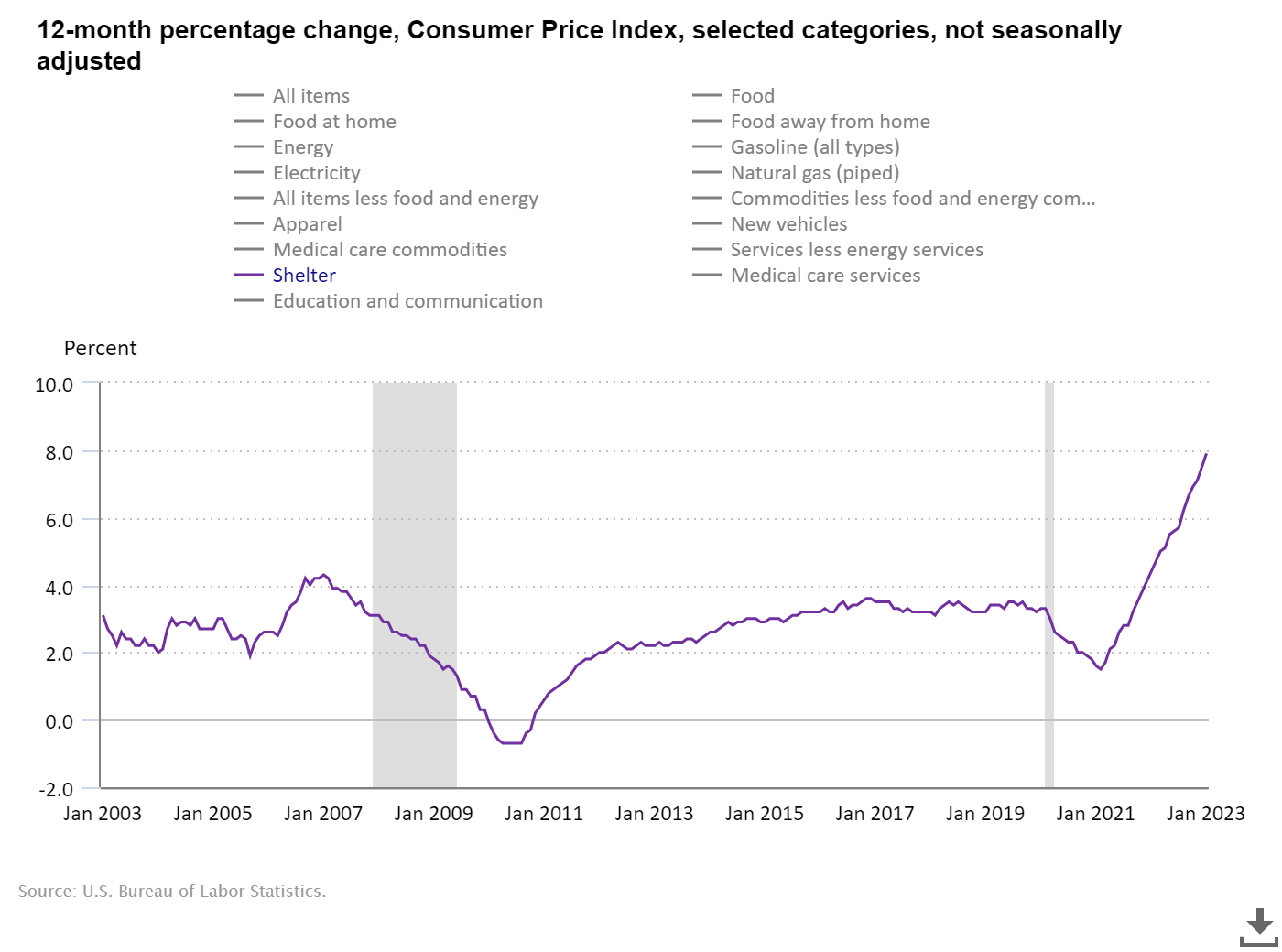

What do we know about inflation? The growth charge is cooling from previous year’s peak, and the shelter inflation portion of housing will great down over time. It is greatly recognized that the CPI inflation shelter data lags a large amount, and given that it is the most important ingredient of main inflation, it’s a large deal.

This is why I went on CNBC final yr to say the development charge of rents falling was a favourable for inflation for 2023. Even so, the CPI details lags badly on this actuality, and the dread was that the Federal Reserve did not understand this.

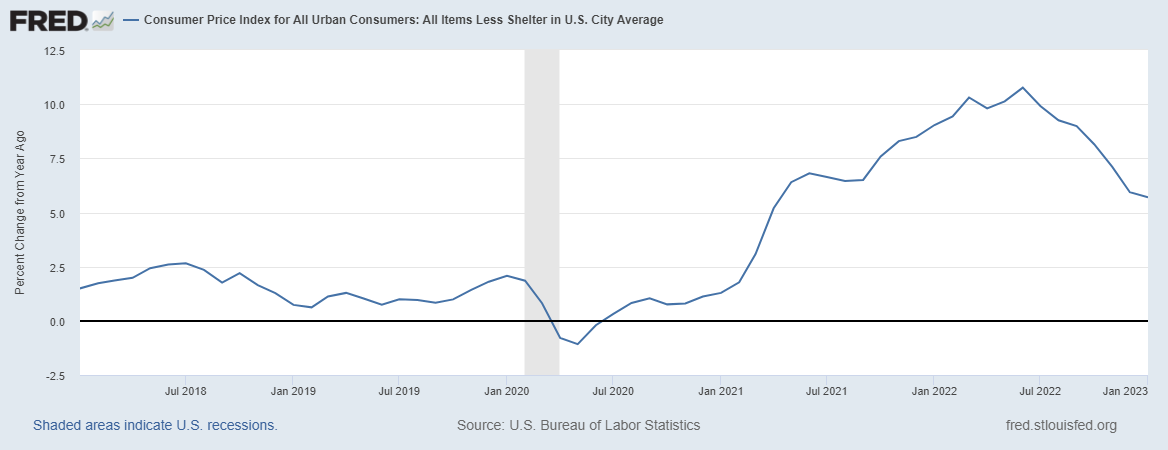

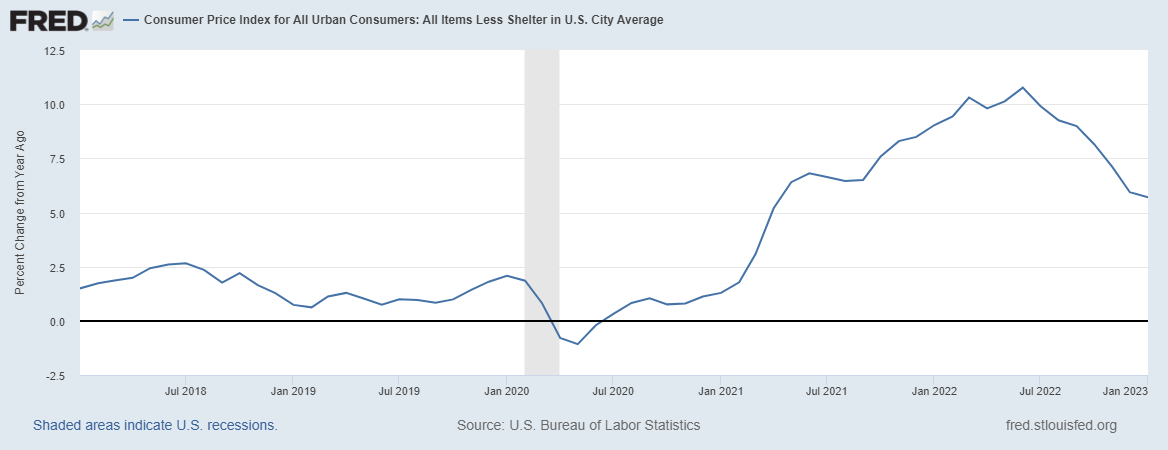

Having said that, then the Federal Reserve truly established a new index that excludes shelter to adapt to the much more present info, which shows the expansion rate of rents is cooling down. Now the Fed focuses on core inflation info, excluding food stuff and strength. Nevertheless, even if I acquire shelter absent and leave foodstuff and vitality inflation in the equation, the advancement price of inflation is cooling additional significantly.

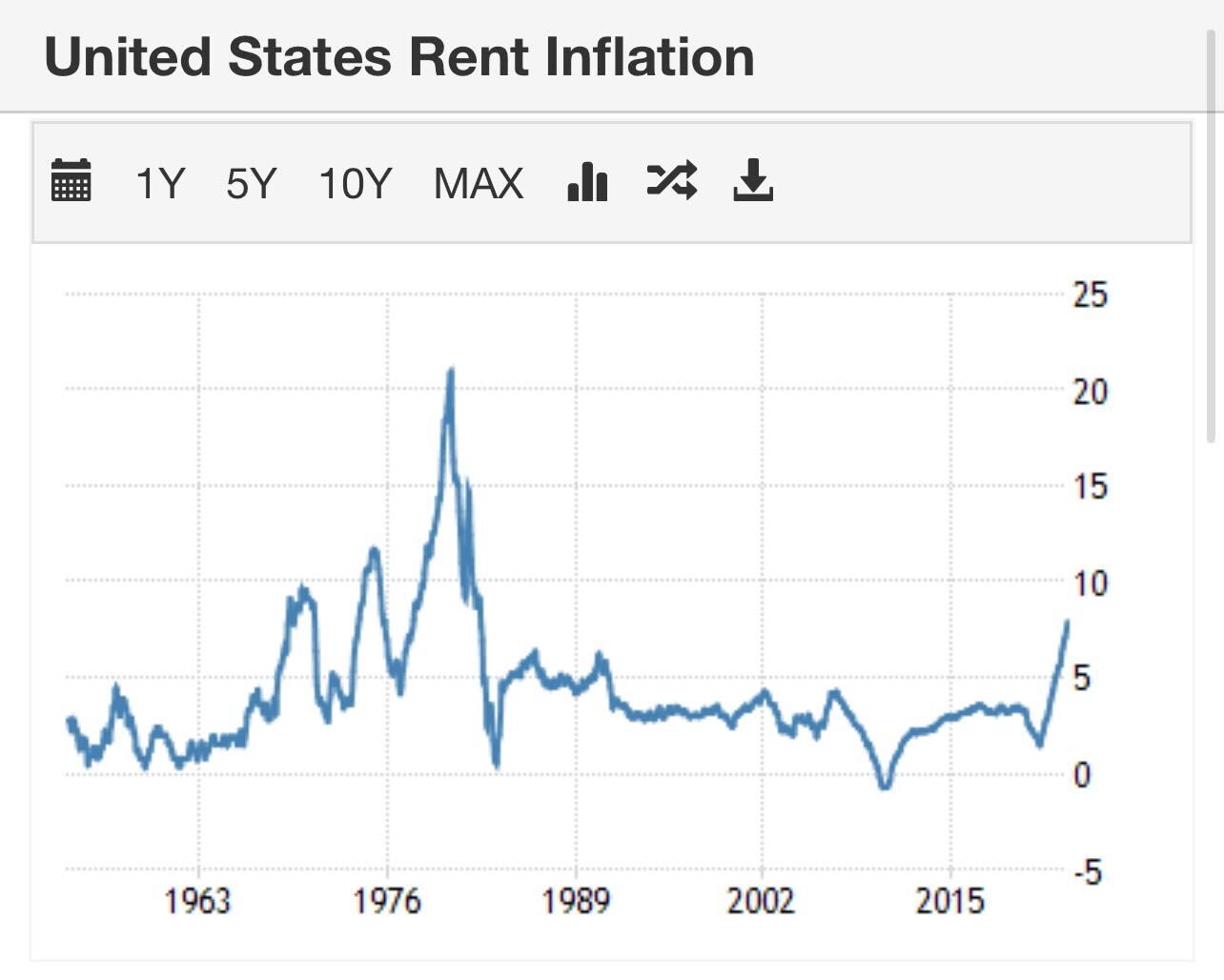

Devoid of lease inflation having off, you can kiss the 1970s inflation comparisons goodbye, and this is why the 10-year yield in no way broke previously mentioned 5.25% — a vital amount for me to even have a considered about 1970s-fashion inflation. As you can see below, the development amount of rents took off a couple of moments again then. After the 1970s, the growth price was stable for many years.

My mentality with inflation information given that October of 2022 has been to give it time: 12 months from now, we will be in a better area. If the financial state went into a task-decline economic downturn, the bond current market would get well ahead of the Fed and home finance loan premiums would tumble speedier. Even so, we aren’t there but.

The Fed pivot will not occur until finally jobless promises break around 323,000 on the four-week moving regular, but the reality is the bond sector is not previous and gradual they will head that way just before the Fed does.

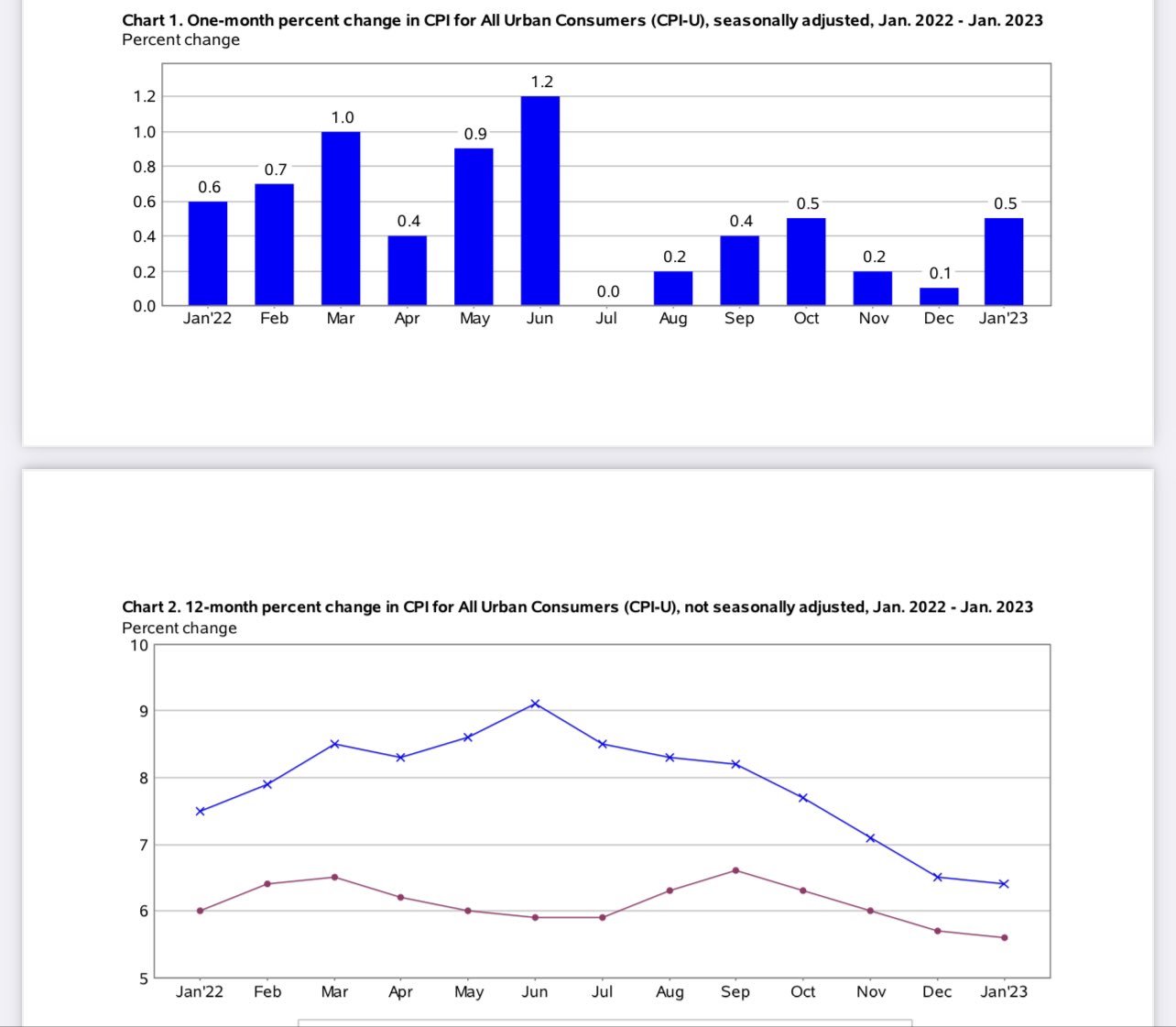

CPI report

From BLS [bolding is mine]: “The Buyer Value Index for All Urban Shoppers (CPI-U) rose .5 percent in January on a seasonally adjusted basis, just after escalating .1 percent in December, the U.S. Bureau of Labor Statistics reported nowadays. In excess of the final 12 months, the all merchandise index elevated 6.4 percent right before seasonal adjustment. The index for shelter was by considerably the major contributor to the regular monthly all goods enhance, accounting for nearly 50 percent of the monthly all things increase, with the indexes for foods, gasoline, and pure gas also contributing.”

As we can see under, the expansion amount of inflation is cooling, but shelter inflation, “Which is lagging genuine-time information,” is retaining the main knowledge increased than it ought to be right now. Keep in mind, you should often aim 12 months out with inflation details and tie it to the weekly economic info. This is why we designed the weekly Housing Marketplace Tracker.

Other rental inflation knowledge shows a amazing-down, popular with global pandemics. Even so, not only is the serious-time knowledge cooling, we have practically 1 million flats that will be crafted in the near long run, and the very best way to deal with inflation is generally much more source.

Hopefully, this clarification of my forecast for 2023, such as the 10-yr generate, home loan premiums, and inflation presents you a improved understanding of why I really do not imagine mortgage prices can increase above past year’s peak of 7.37%.

Now, one particular way mortgage rates could blow previous 7.37% is if the financial state commences to increase yet again, provide doesn’t develop, and wage development, which has been cooling, reverses, and explodes better once again.

If rents and wages took off bigger again, some new war created additional of a supply shock, and the labor industry acquired even tighter, this would counter my discussion that the progress level of inflation has peaked. On the other hand, so significantly, it does not appear like everything I just talked about is going on, so give it a lot more time, and the inflation progress price will reasonable.