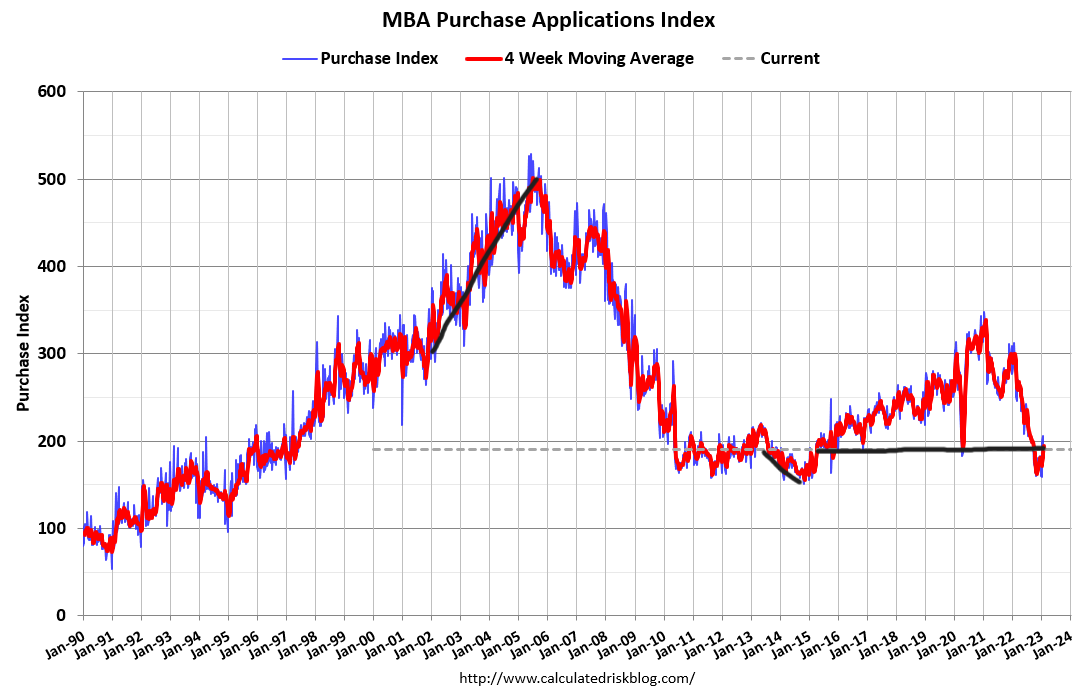

Very last year, we had a historical dive in order application info, but a short while ago we located a base and acquire applications have bounced from the lows. Since Nov. 9, when this knowledge line started out to get much better, and excluding the standard severe slowdown the final and first 7 days of the 12 months, it is been beneficial exterior of one particular 7 days. I am maintaining an eye on how considerably advancement we can get with mortgage loan fees over 6%.

This 7 days, we will get a very good check with the invest in application info as property finance loan charges have risen just lately. I am searching ahead to observing how the facts reacts to greater fees. Contrary to the COVID-19 recovery, which was speedy and sharp, we are now working with a a lot different backdrop. Morgage costs are higher and we’re operating from a great deal increased property selling prices as very well.

The one gain of the housing industry now is that times on the market place are no more time youngsters, which suggests we are finding closer to a far more well balanced market. This indicates consumers have a lot more say now in the property-shopping for course of action. Last but not least, all the constructive facts we have noticed given that Nov. 9 seems ahead 30-90 days, so the present property product sales will clearly show much better info coming up.

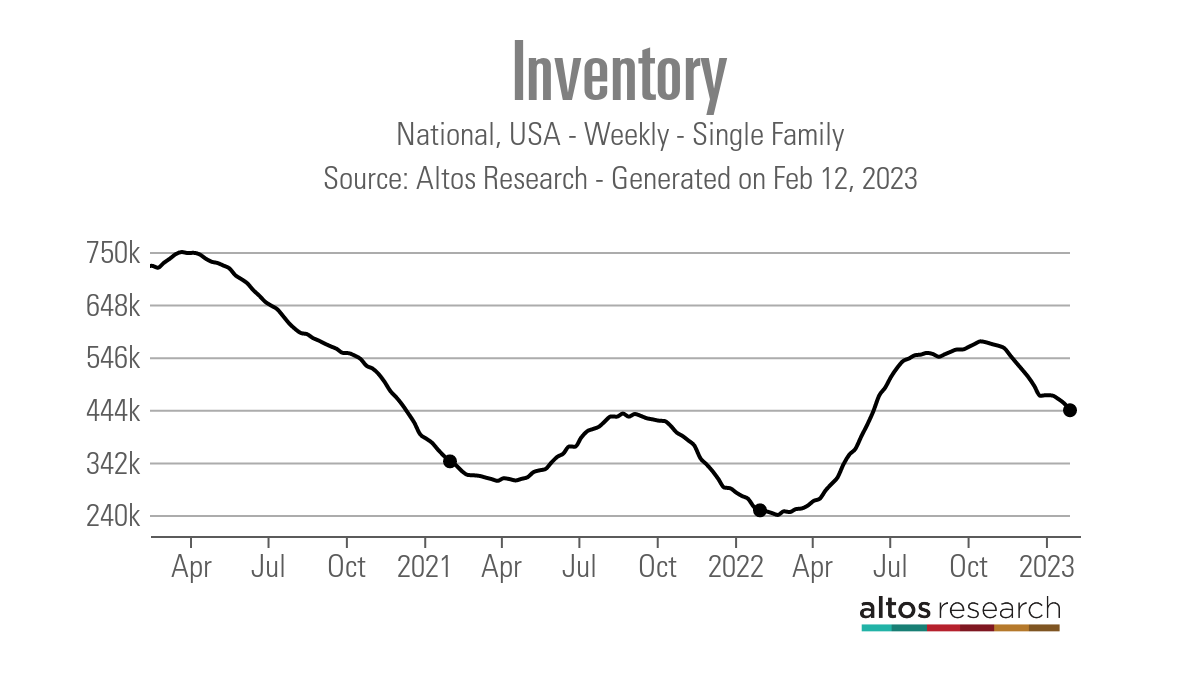

Weekly housing inventory

When I saw a slight enhance in housing inventory in January, I obtained pretty energized for the reason that some of the need collapse we noticed in the 2nd half of 2022 was from people today selecting not to listing their properties because of their anxiety of obtaining yet another. So, when I observed the slight inventory boost, I assumed this was a superior craze.

In advance of 2020, weekly housing inventory bottomed out in the January/February timeframe, and then the seasonal spring enhance would start off. From 2014 to 2016, housing inventory bottomed out in January. From 2017 to 2019, the stock levels in January and February had been incredibly near to each other ahead of the seasonal thrust higher.

Nevertheless, given that 2020, this hasn’t been the situation — stock has tended to bottom out a little later on in the 12 months. In 2021, inventory bottomed out in April, and in 2022 inventory bottomed out in March.

In the final two weeks, housing inventory has been declining significantly and I hope we are coming nearer to the bottom of the seasonal inventory drop. Regretably, last 7 days we observed a larger drop in stock than the former week, as models fell by 13,238 according to Altos Investigate.

So I am crossing my fingers that we are obtaining nearer to the stop of the seasonal stock decrease since the past matter we want to see is bidding wars again, particularly with need performing from substantially decreased degrees than what we saw in 2020/2021, and the early months of 2022. The beneficial component is that inventory is however bigger than past yr

- Weekly stock alter (Feb. 3-Feb. 10): Fell From 456,990 to 443,416

- Exact 7 days final 12 months (Feb. 4-Feb. 11): Fell from 255,662 to 249,161

Because I could see that housing demographics ended up heading to be good in the a long time 2020-2024, I truly didn’t want to see inventory break to all-time lows all through this period of time. This reality made my fear of residence prices overheating, which they did, and once mortgage loan prices rose, the housing sector took an extraordinary affordability hit. Last year, we had a historical dive in housing need and did not get significantly inventory.

Sad to say, we have a very good shot of the subsequent existing household product sales report exhibiting even reduced stock degrees than the 970,000 level we are working with nowadays. This implies 2022 and 2023 are the only moments in the latest record wherever the NAR energetic listing details is under 1 million.

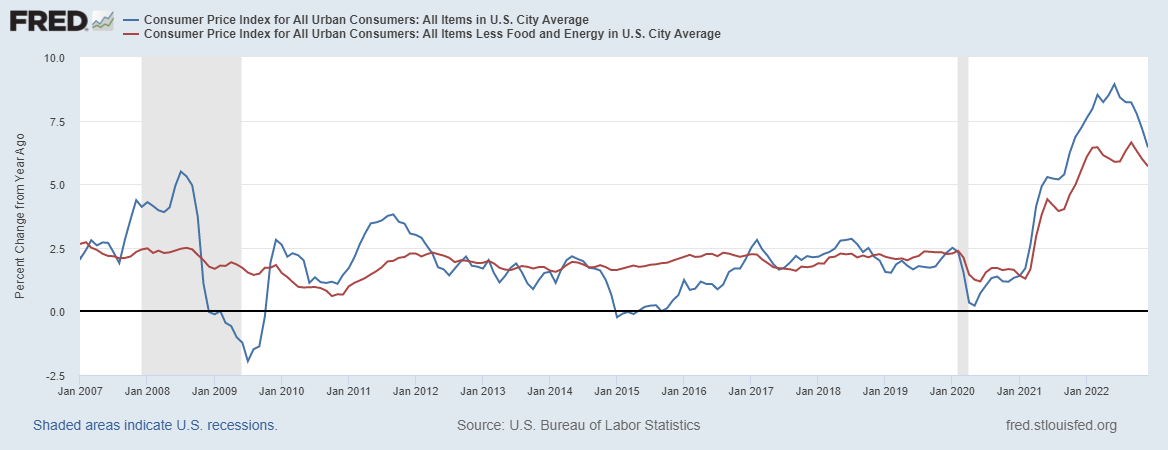

10-calendar year produce and house loan costs

In my 2023 forecast, if the economic climate stayed agency my 10-calendar year produce range was involving 3.21% and 4.25%, equating to house loan premiums staying in a selection of 5.75% to 7.25%. For some time now, I have reviewed how it would be tricky to crack beneath 3.42% with comply with-as a result of bond acquiring, indicating home loan fees would slide even further. The market made a number of attempts to split that amount, but now bond yields have reversed better.

The issue this 7 days with the CPI report data staying launched, is whether or not we will see a W forming in this chart, which would suggest bond yields head back to 4.25%, or no matter whether the downtrend carries on. Above time, the advancement charge of inflation will interesting down the moment rents get accounted for in a a lot more serious-time fashion.

Also, element of the 2023 forecast is that if the labor marketplace breaks, the 10-calendar year generate could get to 2.72%, which would imply mortgage loan charges in the lower 5% selection. And if the spreads get greater, we could even have a 4-manage on mortgage rates. For now, even though, the labor market is nevertheless reliable.

The week ahead

This will be an fascinating week for economic information, bonds and housing. To start with and most important, this week’s purchase software details is important. It will be the initial apps facts amid a half a proportion transfer better in house loan fees, and the next number of weeks will be vital, much too, if charges keep at 6.50% or head larger. Bear in mind, you really should prioritize numbers over people if the tracker info goes destructive, you go with data somewhat than a own belief.

The massive transfer for costs need to be the Buyer Price Index report this week. If it is hotter than envisioned, we could see bonds act negatively to that report. Also, this 7 days we have jobless promises, retail sales, Producer Price tag Index inflation, the homebuilders’ self-assurance survey, housing starts and the Main Financial Index!

It is likely to be a hectic 7 days with economic details that can move the bond marketplace and house loan rates. A person point is specified from the info: mortgage charges heading decrease, even to just 5.99%, shifted the housing sector, which is a little something to don’t forget as we go ahead