The large inflation and double-digit house loan fees of the 1970s and early 1980s look to haunt the Federal Reserve, which would like to great the overall economy and even provoke a career-decline recession to keep away from that state of affairs.

But the most recent Client Price tag Index inflation report shows how the fear of 1970s-design and style inflation is wildly overblown. Today’s figures never glimpse like the 1970s at all, when lease, wages, and oil shocks sent inflation managing hotter than nearly anything we have viewed in new fashionable-working day heritage.

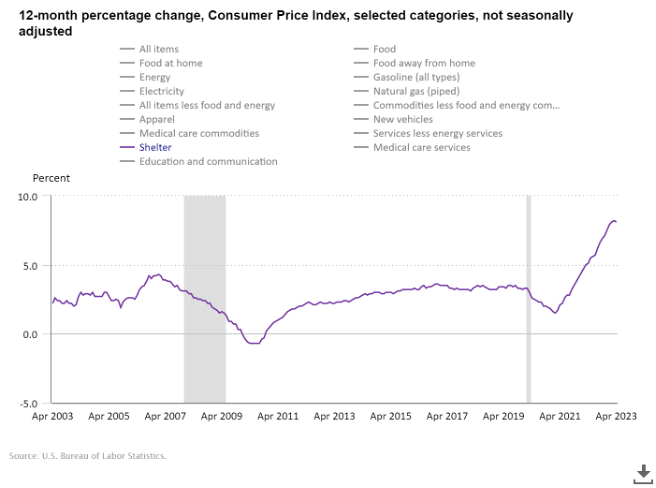

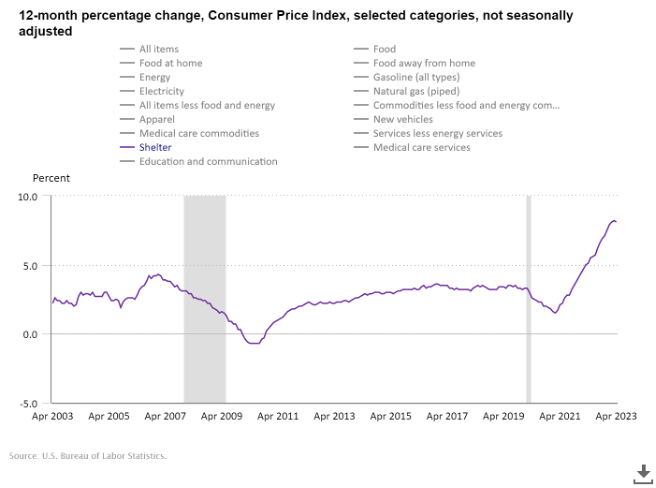

Shelter inflation

Shelter inflation had a gentle lessen print month to month in April. Considering the fact that this information line is the most considerable ingredient of CPI — accounting for 44.4% of the index — the reality that this index is established to gradual down more than the up coming 12 months assures that we will not see the growth in inflation that we observed in 1970s.

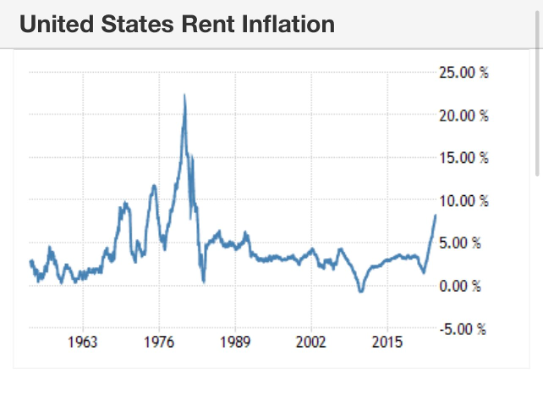

Rent inflation

We don’t will need to get worried about 1970s-type rent inflation. That kind of inflation couldn’t transpire nowadays since the shelter inflation growth rate has been cooling off by now, and we have viewed this in additional actual-time knowledge.

Also, we have above 900,000 condominium units coming on line quickly, and the most effective way to defeat inflation is with extra provide. If you try to defeat inflation by destroying demand, that is only a limited-expression correct. This is outstanding news for mortgage costs, because slipping hire inflation can make a far better scenario for home finance loan prices falling in the next year than rising.

In September on CNBC I talked about how the good story for 2023 would be obvious by the commence of the yr: that the inflation advancement price was likely to neat down, driven by shelter inflation. The inflation data lags, so I realized it would get time, but it happened.

Right now, with enormous charge hikes in the program and a banking crisis building credit history tighter, the outlook for 1970s inflation is on the lookout less and fewer. In truth, it in no way experienced a likelihood.

From the CPI report: The Customer Price tag Index for All Urban Buyers (CPI-U) rose .4 percent in April on a seasonally modified basis right after escalating .1 p.c in March, the U.S. Bureau of Labor Studies reported currently. Above the past 12 months, the all-items index rose 4.9 percent prior to seasonal adjustment.

How did home loan premiums respond?

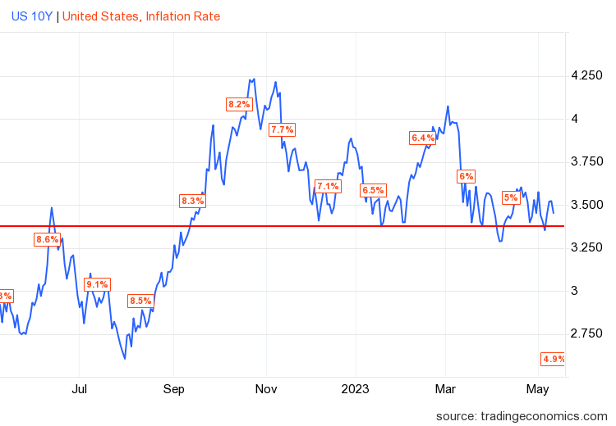

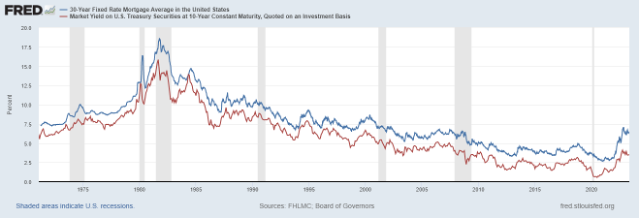

Soon after the report, what did the 10-yr produce do? It fell just as it should really have, but it has still, held the Gandalf line in the sand — the spot concerning 3.37%-3.42%. The chart underneath reveals the 10-yr yield versus the headline year-around-year inflation progress fee. As you can see, we have had a lot lessen yields with hotter inflation details.

However, the 10-year produce seems like it has peaked unless the financial state gets an additional wind and begins expanding considerably quicker. On Oct. 27, I designed the case for reduced home finance loan rates and bond yields in 2023. I imagine the mega-bearish housing camp was counting on the 10-year produce finding towards 5.25%, and with lousy spreads, that would get home loan fees to 8%-10%.

My 2023 forecast for the 10-year yield and home loan prices experienced just one distinct view, the 10-12 months generate really should be among 3.21%-4.25 as very long as the economy stayed business. Remaining organization suggests the labor market does not break and jobless statements, men and women filing for unemployment benefits, stays beneath 323,000 on a four-week transferring typical. I have been much more concentrated on the labor current market this year than the inflation growth fee since I believe that the current market knew inflation was falling.

Of course, the banking disaster has added a new variable to the financial photo this yr. On the other hand, even with that, the labor industry, while having softer, hasn’t broken yet. Home finance loan charges did tumble Wednesday to 6.57%, and which is nevertheless higher than they ought to be because spreads involving the 10-calendar year produce and the 30-yr home finance loan prices are nevertheless traditionally large. If we had normal spreads right now, property finance loan rates would be around all-around 5.25%

Can you all envision the housing sector if home finance loan charges had been at 5.25% currently? The Fed, which has stated it wishes a housing reset, would totally get rid of it. Under that reset, it is older Us residents who can purchase households, not young People in america looking to start off their life. This is 1 purpose you haven’t heard a whisper from the Fed about encouraging the housing market place throughout this time.

Labor sector cooling

The labor market has been cooling just lately, as career openings have fallen practically 2.5 million from the peak in 2022. The Fed doesn’t concern a work-loss recess, and in reality their unemployment amount forecast for 2023 phone calls for one. They imagine they have a deal with right up until job openings tumble a lot extra.

It looks to me that they will be extra comfy with career openings having back to 7 million, which was the place we have been right before COVID-19 hit us. I wrote about the the latest employment report and broke down a ton of labor facts strains that make a difference to my 10-12 months produce mortgage loan rate forecast.

Though the labor market place is cooling, it has not broken nevertheless. If we experienced the 1970s inflation tale, then the mortgage loan charges and bond yields could increase all through a economic downturn as they did again then. On the other hand, as we can see, the bond market place hardly ever bit on the 1970’s inflation premise. Keep in mind, these two enjoys have been gradual dancing given that 1971, and they never cease. Sometimes they are closer to each and every other, and from time to time they’re farther apart. However, they are constantly jointly.

In general, the CPI report did not have far too numerous surprises, even however the headline selection was decreased than some expected. With the Federal Reserve, they’re hunting at inflation without the need of the shelter part since that knowledge line lags and services inflation has been company lately.

However, the tale is established in stone: the Fed wants its recession since it will be a badge of honor for them when they go off into the afterlife, as Paul Volcker has. They selected to hike charges far more even although they knew credit score was finding tighter and the banking crisis may possibly help them strike their inflation focus on.

So, the truth is, what does the Fed do when the labor marketplace breaks, with headline inflation on the lookout like this? We are observing the expansion charge unwind, and now the most major variable in CPI will have a 12-thirty day period cooling-down tour.

This is why tracking weekly housing details will be extra important than ever this calendar year. I do not just observe housing knowledge, my principal occupation is to keep track of financial cycles very first and housing is a secondary information line. With all the drama we have going on in 2023, the rest of the yr will get thrilling week to 7 days.